How and when: ridge regression with glmnet

@drsimonj here to show you how to conduct ridge regression (linear regression with L2 regularization) in R using the glmnet package, and use simulations to demonstrate its relative advantages over ordinary least squares regression.

Ridge regression

Ridge regression uses L2 regularisation to weight/penalise residuals when the parameters of a regression model are being learned. In the context of linear regression, it can be compared to Ordinary Least Square (OLS). OLS defines the function by which parameter estimates (intercepts and slopes) are calculated. It involves minimising the sum of squared residuals. L2 regularisation is a small addition to the OLS function that weights residuals in a particular way to make the parameters more stable. The outcome is typically a model that fits the training data less well than OLS but generalises better because it is less sensitive to extreme variance in the data such as outliers.

Packages

We’ll make use of the following packages in this post:

library(tidyverse)

library(broom)

library(glmnet)

Ridge regression with glmnet

The glmnet package provides the functionality for ridge regression viaglmnet(). Important things to know:

- Rather than accepting a formula and data frame, it requires a vector input and matrix of predictors.

- You must specify

alpha = 0for ridge regression. - Ridge regression involves tuning a hyperparameter, lambda.

glmnet()will generate default values for you. Alternatively, it is common practice to define your own with thelambdaargument (which we’ll do).

Here’s an example using the mtcars data set:

y <- mtcars$hp

x <- mtcars %>% select(mpg, wt, drat) %>% data.matrix()

lambdas <- 10^seq(3, -2, by = -.1)

fit <- glmnet(x, y, alpha = 0, lambda = lambdas)

summary(fit)

#> Length Class Mode

#> a0 51 -none- numeric

#> beta 153 dgCMatrix S4

#> df 51 -none- numeric

#> dim 2 -none- numeric

#> lambda 51 -none- numeric

#> dev.ratio 51 -none- numeric

#> nulldev 1 -none- numeric

#> npasses 1 -none- numeric

#> jerr 1 -none- numeric

#> offset 1 -none- logical

#> call 5 -none- call

#> nobs 1 -none- numeric

Because, unlike OLS regression done with lm(), ridge regression involves tuning a hyperparameter, lambda, glmnet() runs the model many times for different values of lambda. We can automatically find a value for lambda that is optimal by using cv.glmnet() as follows:

cv_fit <- cv.glmnet(x, y, alpha = 0, lambda = lambdas)

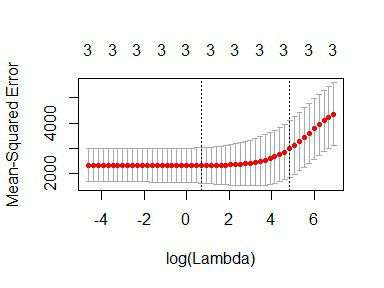

cv.glmnet() uses cross-validation to work out how well each model generalises, which we can visualise as:

plot(cv_fit)

The lowest point in the curve indicates the optimal lambda: the log value of lambda that best minimised the error in cross-validation. We can extract this values as:

opt_lambda <- cv_fit$lambda.min

opt_lambda

#> [1] 3.162278

And we can extract all of the fitted models (like the object returned byglmnet()) via:

fit <- cv_fit$glmnet.fit

summary(fit)

#> Length Class Mode

#> a0 51 -none- numeric

#> beta 153 dgCMatrix S4

#> df 51 -none- numeric

#> dim 2 -none- numeric

#> lambda 51 -none- numeric

#> dev.ratio 51 -none- numeric

#> nulldev 1 -none- numeric

#> npasses 1 -none- numeric

#> jerr 1 -none- numeric

#> offset 1 -none- logical

#> call 5 -none- call

#> nobs 1 -none- numeric

These are the two things we need to predict new data. For example, predicting values and computing an R2 value for the data we trained on:

y_predicted <- predict(fit, s = opt_lambda, newx = x)

# Sum of Squares Total and Error

sst <- sum(y^2)

sse <- sum((y_predicted - y)^2)

# R squared

rsq <- 1 - sse / sst

rsq

#> [1] 0.9318896

The optimal model has accounted for 93% of the variance in the training data.

Ridge v OLS simulations

By producing more stable parameters than OLS, ridge regression should be less prone to overfitting training data. Ridge regression might, therefore, predict training data less well than OLS, but better generalise to new data. This will particularly be the case when extreme variance in the training data is high, which tends to happen when the sample size is low and/or the number of features is high relative to the number of observations.

Below is a simulation experiment I created to compare the prediction accuracy of ridge regression and OLS on training and test data.

I first set up the functions to run the simulation:

# Compute R^2 from true and predicted values

rsquare <- function(true, predicted) {

sse <- sum((predicted - true)^2)

sst <- sum(true^2)

rsq <- 1 - sse / sst

# For this post, impose floor...

if (rsq < 0) rsq <- 0

return (rsq)

}

# Train ridge and OLS regression models on simulated data set with `n_train`

# observations and a number of features as a proportion to `n_train`,

# `p_features`. Return R squared for both models on:

# - y values of the training set

# - y values of a simualted test data set of `n_test` observations

# - The beta coefficients used to simulate the data

ols_vs_ridge <- function(n_train, p_features, n_test = 200) {

## Simulate datasets

n_features <- floor(n_train * p_features)

betas <- rnorm(n_features)

x <- matrix(rnorm(n_train * n_features), nrow = n_train)

y <- x %*% betas + rnorm(n_train)

train <- data.frame(y = y, x)

x <- matrix(rnorm(n_test * n_features), nrow = n_test)

y <- x %*% betas + rnorm(n_test)

test <- data.frame(y = y, x)

## OLS

lm_fit <- lm(y ~ ., train)

# Match to beta coefficients

lm_betas <- tidy(lm_fit) %>%

filter(term != "(Intercept)") %>%

{.$estimate}

lm_betas_rsq <- rsquare(betas, lm_betas)

# Fit to training data

lm_train_rsq <- glance(lm_fit)$r.squared

# Fit to test data

lm_test_yhat <- predict(lm_fit, newdata = test)

lm_test_rsq <- rsquare(test$y, lm_test_yhat)

## Ridge regression

lambda_vals <- 10^seq(3, -2, by = -.1) # Lambda values to search

cv_glm_fit <- cv.glmnet(as.matrix(train[,-1]), train$y, alpha = 0, lambda = lambda_vals, nfolds = 5)

opt_lambda <- cv_glm_fit$lambda.min # Optimal Lambda

glm_fit <- cv_glm_fit$glmnet.fit

# Match to beta coefficients

glm_betas <- tidy(glm_fit) %>%

filter(term != "(Intercept)", lambda == opt_lambda) %>%

{.$estimate}

glm_betas_rsq <- rsquare(betas, glm_betas)

# Fit to training data

glm_train_yhat <- predict(glm_fit, s = opt_lambda, newx = as.matrix(train[,-1]))

glm_train_rsq <- rsquare(train$y, glm_train_yhat)

# Fit to test data

glm_test_yhat <- predict(glm_fit, s = opt_lambda, newx = as.matrix(test[,-1]))

glm_test_rsq <- rsquare(test$y, glm_test_yhat)

data.frame(

model = c("OLS", "Ridge"),

betas_rsq = c(lm_betas_rsq, glm_betas_rsq),

train_rsq = c(lm_train_rsq, glm_train_rsq),

test_rsq = c(lm_test_rsq, glm_test_rsq)

)

}

# Function to run `ols_vs_ridge()` `n_replications` times

repeated_comparisons <- function(..., n_replications = 5) {

map(seq(n_replications), ~ ols_vs_ridge(...)) %>%

map2(seq(.), ~ mutate(.x, replicate = .y)) %>%

reduce(rbind)

}

Now run the simulations for varying numbers of training data and relative proportions of features (takes some time):

d <- purrr::cross_d(list(

n_train = seq(20, 200, 20),

p_features = seq(.55, .95, .05)

))

d <- d %>%

mutate(results = map2(n_train, p_features, repeated_comparisons))

Visualise the results…

For varying numbers of training data (averaging over number of features), how well do both models predict the training and test data?

d %>%

unnest() %>%

group_by(model, n_train) %>%

summarise(

train_rsq = mean(train_rsq),

test_rsq = mean(test_rsq)) %>%

gather(data, rsq, contains("rsq")) %>%

mutate(data = gsub("_rsq", "", data)) %>%

ggplot(aes(n_train, rsq, color = model)) +

geom_line() +

geom_point(size = 4, alpha = .3) +

facet_wrap(~ data) +

theme_minimal() +

labs(x = "Number of training observations",

y = "R squared")

As hypothesised, OLS fits the training data better but Ridge regression better generalises to new test data. Further, these effects are more pronounced when the number of training observations is low.

For varying relative proportions of features (averaging over numbers of training data) how well do both models predict the training and test data?

d %>%

unnest() %>%

group_by(model, p_features) %>%

summarise(

train_rsq = mean(train_rsq),

test_rsq = mean(test_rsq)) %>%

gather(data, rsq, contains("rsq")) %>%

mutate(data = gsub("_rsq", "", data)) %>%

ggplot(aes(p_features, rsq, color = model)) +

geom_line() +

geom_point(size = 4, alpha = .3) +

facet_wrap(~ data) +

theme_minimal() +

labs(x = "Number of features as proportion\nof number of observation",

y = "R squared")

Again, OLS has performed slightly better on training data, but Ridge better on test data. The effects are more pronounced when the number of features is relatively high compared to the number of training observations.

The following plot helps to visualise the relative advantage (or disadvantage) of Ridge to OLS over the number of observations and features:

d %>%

unnest() %>%

group_by(model, n_train, p_features) %>%

summarise(train_rsq = mean(train_rsq),

test_rsq = mean(test_rsq)) %>%

group_by(n_train, p_features) %>%

summarise(RidgeAdvTrain = train_rsq[model == "Ridge"] - train_rsq[model == "OLS"],

RidgeAdvTest = test_rsq[model == "Ridge"] - test_rsq[model == "OLS"]) %>%

gather(data, RidgeAdvantage, contains("RidgeAdv")) %>%

mutate(data = gsub("RidgeAdv", "", data)) %>%

ggplot(aes(n_train, p_features, fill = RidgeAdvantage)) +

scale_fill_gradient2(low = "red", high = "green") +

geom_tile() +

theme_minimal() +

facet_wrap(~ data) +

labs(x = "Number of training observations",

y = "Number of features as proportion\nof number of observation") +

ggtitle("Relative R squared advantage of Ridge compared to OLS")

This shows the combined effect: that Ridge regression better transfers to test data when the number of training observations is low and/or the number of features is high relative to the number of training observations. OLS performs slightly better on the training data under similar conditions, indicating that it is more prone to overfitting training data than when ridge regularisation is employed.

Sign off

Thanks for reading and I hope this was useful for you.

For updates of recent blog posts, follow @drsimonj on Twitter, or email me atdrsimonjackson@gmail.com to get in touch.

If you’d like the code that produced this blog, check out the blogR GitHub repository.

转自:https://drsimonj.svbtle.com/ridge-regression-with-glmnet

How and when: ridge regression with glmnet的更多相关文章

- ISLR系列:(4.2)模型选择 Ridge Regression & the Lasso

Linear Model Selection and Regularization 此博文是 An Introduction to Statistical Learning with Applicat ...

- Ridge Regression(岭回归)

Ridge Regression岭回归 数值计算方法的"稳定性"是指在计算过程中舍入误差是可以控制的. 对于有些矩阵,矩阵中某个元素的一个很小的变动,会引起最后计算结果误差很大,这 ...

- support vector regression与 kernel ridge regression

前一篇,我们将SVM与logistic regression联系起来,这一次我们将SVM与ridge regression(之前的linear regression)联系起来. (一)kernel r ...

- Jordan Lecture Note-4: Linear & Ridge Regression

Linear & Ridge Regression 对于$n$个数据$\{(x_1,y_1),(x_2,y_2),\cdots,(x_n,y_n)\},x_i\in\mathbb{R}^d,y ...

- Ridge Regression and Ridge Regression Kernel

Ridge Regression and Ridge Regression Kernel Reference: 1. scikit-learn linear_model ridge regressio ...

- 再谈Lasso回归 | elastic net | Ridge Regression

前文:Lasso linear model实例 | Proliferation index | 评估单细胞的增殖指数 参考:LASSO回歸在生物醫學資料中的簡單實例 - 生信技能树 Linear le ...

- 岭回归(Ridge Regression)

一.一般线性回归遇到的问题 在处理复杂的数据的回归问题时,普通的线性回归会遇到一些问题,主要表现在: 预测精度:这里要处理好这样一对为题,即样本的数量和特征的数量 时,最小二乘回归会有较小的方差 时, ...

- Kernel ridge regression(KRR)

作者:桂. 时间:2017-05-23 15:52:51 链接:http://www.cnblogs.com/xingshansi/p/6895710.html 一.理论描述 Kernel ridg ...

- 机器学习方法:回归(二):稀疏与正则约束ridge regression,Lasso

欢迎转载,转载请注明:本文出自Bin的专栏blog.csdn.net/xbinworld. "机器学习方法"系列,我本着开放与共享(open and share)的精神撰写,目的是 ...

随机推荐

- 用C#写经理评分系统

先写需求: 01.显示员工信息 02.实现项目经理给员工评分的功能 第一步: 建立两个类,员工类和项目经理类 定义属性和方法 员工类:工号.年龄.姓名.人气值.项 ...

- NOIP2014D2T2寻找道路

洛谷传送门 这道题可以把边都反着存一遍,从终点开始深搜,然后把到不了的点 和它们所指向的点都去掉. 最后在剩余的点里跑一遍spfa就可以了. --代码 #include <cstdio> ...

- spring之注解

1.@Autowired 可以对成员变量.方法和构造函数进行自动配置(根据类型进行自动装配) public class UserImpl implements User { @Autowired pr ...

- python scrapy 抓取脚本之家文章(scrapy 入门使用简介)

老早之前就听说过python的scrapy.这是一个分布式爬虫的框架,可以让你轻松写出高性能的分布式异步爬虫.使用框架的最大好处当然就是不同重复造轮子了,因为有很多东西框架当中都有了,直接拿过来使用就 ...

- Aggregate累加器

今天看东西的时候看见这么个扩展方法Aggregate(累加器)很是陌生,于是乎查了查,随手记录一下.直接看一个最简答的版本,其他版本基本没什么区别,需要的时候可看一下 public static TS ...

- App内切换语言

前几天客户提需求,对App增加一个功能,这个功能目前市面上已经很常见,那就是应用内切换语言.啥意思,就是 英.中.法.德.日...语言随意切换. (本案例采用Data-Bingding模式,麻麻再也不 ...

- 【从无到有】JavaScript新手教程——1.简介、变量和运算符

今天带大家来学习一下在网页制作过程中很常用的JavaScript(简称JS). 一.JS的作用: 表单验证,减轻服务端的压力 添加页面动画效果 动态更改页面内容 Ajax网络请求 二.[使用JS的 ...

- MySQL之改_update

MySQL增删改查之改_update UPDATE语句 进行数据记录的更新. 1.更新单个表中的值 语法: UPDATE [IGNORE] table_reference SET col_name1= ...

- VueJS实现一个货币结算自定义控件

Vue.component('currency-input', { template: '\ <div>\ <label v-if="label">{{ l ...

- 分布式锁与实现(二)——基于ZooKeeper实现

引言 ZooKeeper是一个分布式的,开放源码的分布式应用程序协调服务,是Google的Chubby一个开源的实现,是Hadoop和Hbase的重要组件.它是一个为分布式应用提供一致性服务的软件,提 ...